The US stock market pushed higher on April 22, with the Nasdaq Composite setting a new intraday record. Meanwhile, the S&P 500 reclaimed 7,100 as technology led the session.

Three forces lifted the rally. In each case, the driver ties back to the same pivot. A geopolitical overhang lifting just as institutional positioning and corporate results align behind the move higher.

1. US-Iran Ceasefire Extension Removes the Geopolitical Drag

President Trump announced an indefinite extension of the US-Iran ceasefire, reversing the overhang that sent major indexes lower on April 21. Previously, the S&P 500 had closed down 0.63% amid concerns over the ceasefire’s expiry and paused diplomatic talks.

The announcement removes the single largest macro variable pressuring equities this week. Consequently, investors are rotating back into risk assets, supported by a softer dollar and easing oil prices.

2. Hedge Funds Pile Into Tech at a Five-Year High

Hedge fund positioning turned sharply into technology last week, according to Goldman Sachs Prime Book data shared by The Kobeissi Letter. Information Technology names were purchased for the first time in five weeks, led by semiconductors and software. As a result, hedge fund gross and net exposure to global tech now sits at 28.3% and 34.0%, both five-year highs.

However, the contrast matters. According to Bank of America data shared by Walter Bloomberg, active funds sold $15.4 billion in US stocks during March, with technology seeing the largest selling.

Meanwhile, US equity outflows over the past 12 months have reached $284 billion as managers shifted capital into Europe and Japan. In other words, today’s hedge fund bid is fighting that structural current rather than flowing with it.

Still, the tactical side is winning out today. Technology led all sectors with a 1.75% gain, with Broadcom (AVGO) up 4.21%, Micron Technology (MU) surging 6.87%, and Apple (AAPL) climbing 2.53%.

3. Earnings Strength Reinforces a Resilient Economy

GE Vernova (GEV) rose 11.73% after reporting Q1 orders up 71%, raised 2026 guidance, and a beat on both profit and revenue. Similarly, Boeing (BA) climbed 4.84% after a narrower Q1 loss and a record $695 billion backlog.

The two beats span industrials and aerospace, reinforcing that corporate demand held up through Q1 geopolitical noise. Consequently, investors gain a fundamental floor under today’s rally, making the ceasefire relief move harder to fade on earnings-week concerns.

What Happened to Major US Indexes?

At press time, all three major indexes trade higher.

- S&P 500 gained 50.57 points (+0.72%) to 7,114.58

- Nasdaq Composite rose 280.88 points (+1.16%) to 24,540.80, a new intraday record

- Dow Jones Industrial Average added 269.20 points (+0.55%) to 49,418.60

Market breadth leans positive. Advancers accounted for 54.1% of issues while decliners made up 42.1%. Moreover, about 61.8% of stocks traded above their 50-day Simple Moving Average (SMA). SMA is a trend indicator that smooths price data by averaging closing prices over a set period.

The S&P 500 daily chart shows a bull flag forming after a 13.14% pole.The pole formed post the rally from the March 30 low to mid-April peak at 7,147.24. Notably, the pole was built on the post-Iran-war recovery, making the flag’s resolution a direct reflection of whether ceasefire optimism can sustain against the structural outflow backdrop.

A daily close above 7,147.24 would confirm the breakout and open a measured move toward 7,563.34, with the full pole projection pointing toward 8,088.47. Conversely, a drop below 7,049.22 weakens the flag, with 6,741.41 as the next support for the US stock market.

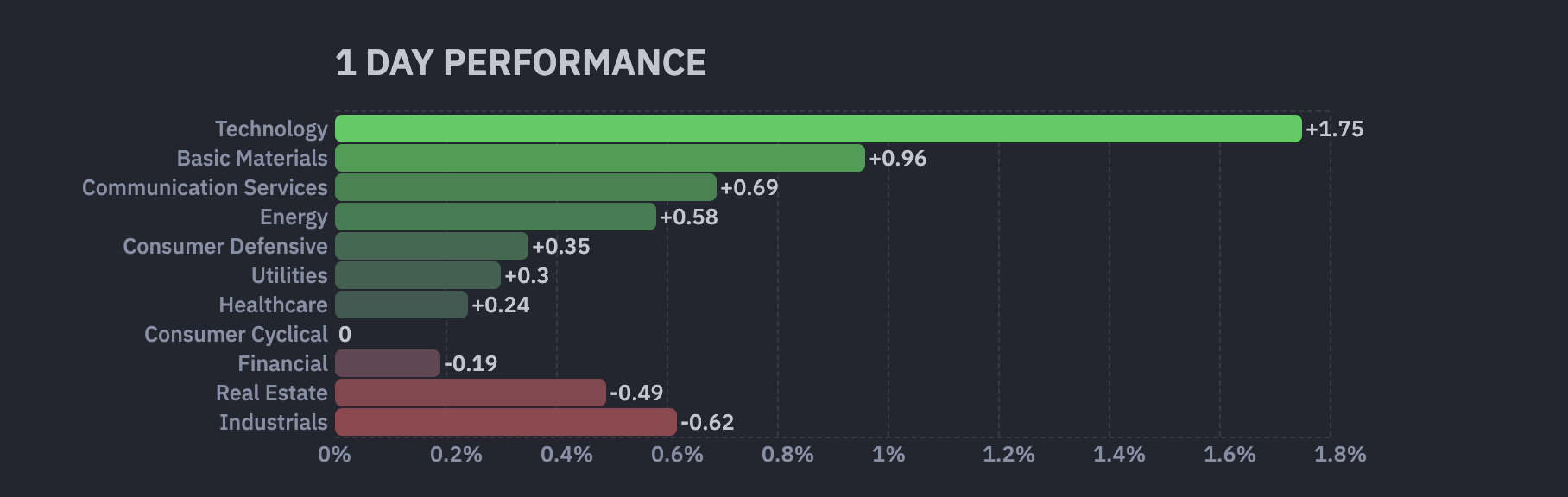

Which Sectors Are Holding Up?

Technology led with +1.75%. Semiconductor demand tied to AI infrastructure anchors the sector, yet the gains will need follow-through to overcome the structural selling pressure.

Basic Materials followed with +0.96%, helped by a softer US Dollar Index (DXY) that supports commodity prices. Communication Services added +0.69%, with Google and Meta benefiting from the same risk-on rotation lifting long-duration growth names as inflation tail risks ease.

Healthcare posted a quieter +0.24%, consistent with the defensive tilt in recent fund flows.

Which Sectors Are Falling?

Industrials led losses at -0.62%. GE Aerospace fell 4.98% and RTX Corporation (RTX) dropped 3.61%. This reflected profit-taking in the defense subsector after it ran hard on Iran headlines.

In effect, this is the mirror image of the same macro driver lifting the rest of the market. Meanwhile, Real Estate declined -0.49% as Treasury yields drifted higher. Financials slipped -0.19%, with Bank of America (BAC) off 0.66% and JPMorgan Chase (JPM) down 0.20% as capital rotated toward growth sectors and banks drifted on pre-FOMC positioning.

Major Stock News Investors Are Watching

Boston Scientific (BSX) advanced roughly 9% despite cutting its 2026 growth outlook, with investors focusing on the Q1 beat rather than the forward guidance revision.

In contrast, United Airlines (UAL) declined despite beating Q1 estimates, as elevated jet fuel costs pressured margins and forward outlook.

Meanwhile, Best Buy (BBY) fell 5.17% after announcing its CEO will step down, the leadership uncertainty outweighing the broader risk-on tone.

What Are Investors Watching Next?

The S&P 500 at 7,147.24 is the immediate test. However, a rejection shifts focus to whether the tactical tech bid can hold against the structural US outflows.

Meanwhile, the FOMC meeting on April 28-29 is the next major catalyst. A dovish tilt could narrow the US underweight, while a hawkish tone would reinforce the rotation into Europe and Japan.

The post Why Is The US Stock Market Up Today? appeared first on BeInCrypto.

Markets,Editor’s Pick,Stock Market News,US Politics#Stock #Market #Today1776886050

{kind=link}