In brief

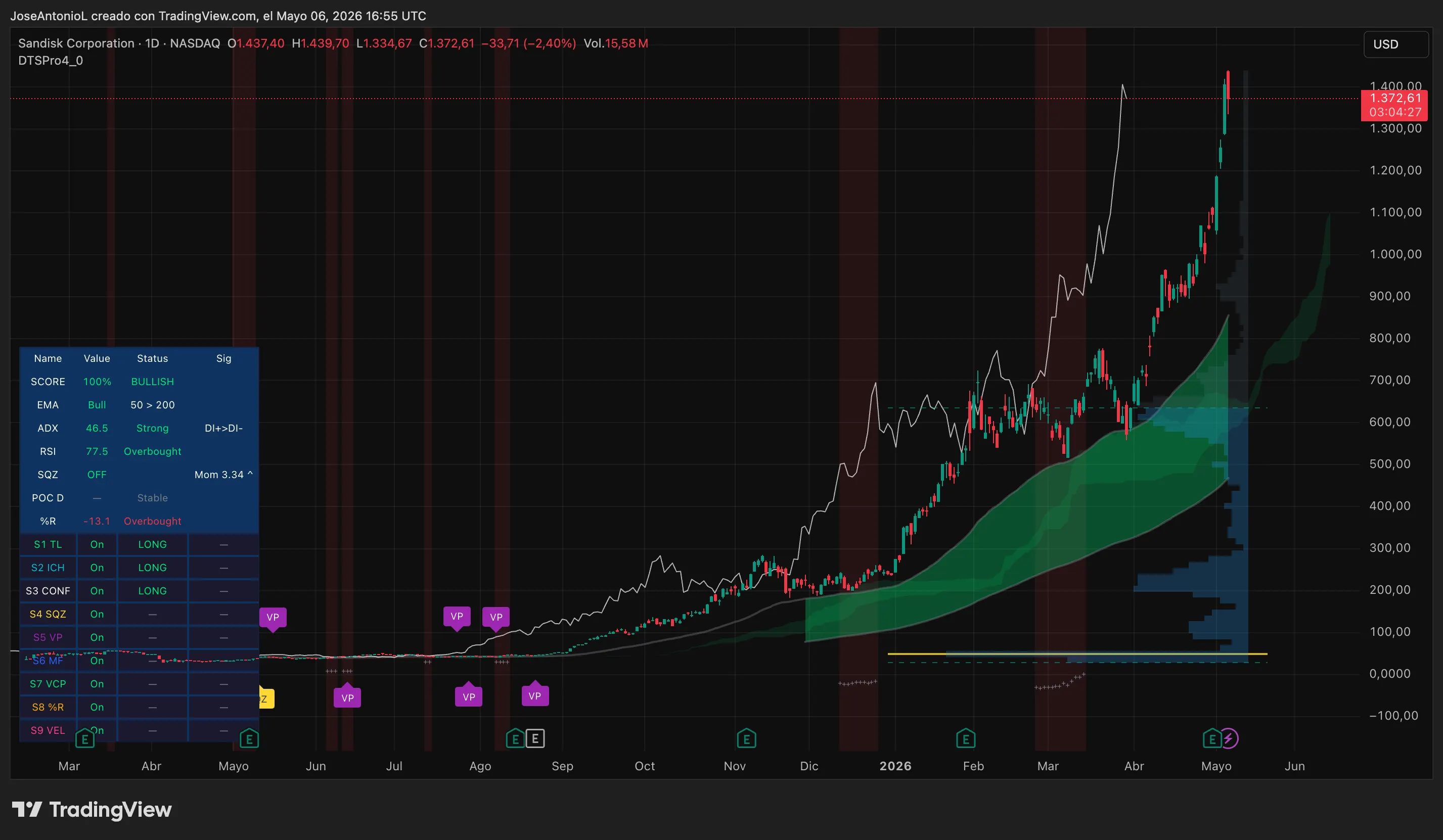

- Sandisk shares have surged 3,314% in the past year, from $32.11 to over $1,096, powered by a global NAND flash shortage and accelerating AI infrastructure spending.

- Per Sandisk’s earnings release, Q3 FY2026 revenue hit $5.95 billion—up 251% year over year—with gross margins expanding from 22.5% to 78.4% in a single year.

- NAND flash prices rose 60% in Q1 2026 and are projected to jump another 70–75% in Q2, with supply expected to remain tight through 2028.

You know a stock is having a moment when it starts outperforming Bitcoin on a year-over-year basis.

Sandisk, which trades publicly as SNDK, has surged from $32.11 to over $1,096 in the past year—a gain of 3,314%. That’s not a typo. The company that put a USB stick in your laptop bag is now one of the most impressive momentum stories in semiconductor history.

The stock is up nearly 500% in 2026 alone.

So what happened? Three things broke in Sandisk’s favor at almost exactly the same time, and together, they turned a storage company into an AI infrastructure play.

The spinoff nobody fully priced in

Sandisk spent nearly a decade buried inside Western Digital. Western Digital completed its $19 billion acquisition of Sandisk in May 2016, aiming to build a storage titan straddling both hard disk drives and NAND flash memory drives. Instead, the two businesses fought each other for capital for years. Activist investors, led by Elliott Management, eventually had enough. The board agreed.

On February 24, 2025, Sandisk completed its tax-free spinoff from Western Digital and relisted on Nasdaq under its own ticker. Western Digital shareholders received one share of SNDK for every three shares of Western Digital held. The spinoff freed Sandisk to operate as a pure-play NAND flash company—no hard disk drag, no conglomerate discount.

The timing was almost absurdly good. Sandisk went public just as the NAND industry was clawing out of one of its worst down-cycles in history—a period when oversupply crashed NAND prices by as much as 60% and pushed every major producer into loss territory. The only way from there was up.

AI is hungry, and NAND is the food

Training and running AI models doesn’t just need compute. It needs storage. A lot of it. And the AI infrastructure buildout—which Nvidia CEO Jensen Huang has called “the largest infrastructure buildout in human history,” is consuming NAND flash at a pace the market never anticipated.

On-device AI in smartphones and PCs requires ever-larger local storage. As devices get more capable, the results they produce also tend to occupy more memory: more megapixels, larger AI models, AI generations with more resolution, high fidelity songs, 4k and even 8k resolution movies, and so on.

Market research firm TrendForce expects the 128GB Android configuration to vanish by the end of 2026 as handsets need more room for local AI processing. The demand shock hit from every direction at once.

Meanwhile, the supply side didn’t keep up. NAND prices rose 60% in Q1 2026, with projections of ending 2026 with a 234% increase per Gartner’s estimations cited by Motley Fool. Supply is expected to remain constrained through 2028.

AI is causing a chip shortage on a scale comparable to what Bitcoin miners did a few years ago—likely even more so.

Sandisk, as one of only a handful of companies operating large-scale NAND operations—including its joint venture with Kioxia in Japan—is sitting directly in the path of that pricing wave. Per Sandisk’s SEC filing, gross margins expanded from 22.5% to 78.4% in a single year. That kind of expansion in a commodity hardware business is practically unheard of.

The numbers are not normal

Sandisk’s fiscal Q3 2026 results, per the company’s earnings release on April 30, were the kind of report that reshapes analyst models. Revenue came in at $5.95 billion, “up 97% sequentially and above the guidance range,” as Sandisk explains. Datacenter revenue hit $1.47 billion, up 645% year over year. Non-GAAP EPS came in at $23.41, against a consensus estimate of $14.66, per Investing.com.

CEO David Goeckeler called the results “a fundamental inflection point for Sandisk.”

Q4 guidance landed at $7.75–$8.25 billion in revenue with non-GAAP gross margin of 79–81%, per the same release. That’s more revenue in a single quarter than most semiconductor companies see in an entire year.

And everything seems to be working in favor of Sandisk.

The company retired $650 million in long-term debt last quarter, leaving it with zero long-term debt, and authorized a share buyback program, per 24/7 Wall St. It then joined the Nasdaq-100 on April, replacing Atlassian, forcing passive index funds to absorb shares into their holdings on top of an already parabolic chart.

It’s also closing big multi-year supply agreements with partners that the company qualifies as “higher-value customers.”

In earnings-call language, that means hyperscalers. So, if Nvidia is the de facto computing provider of the AI space, Sandisk wants to become its de facto storage provider. The task is not as easy—Nvidia’s CUDA technology gives it an advantage that locks developers in its ecosystem—but is also not impossible to achieve.

The risk worth considering

The Sandisk rally, though, may be overheating. The price-to-earnings ratio sits at 41x trailing earnings, well above Sandisk’s five-year median of 15.74x. Some traders may be rotating gains out of SNDK into other names, a potential momentum-exhaustion signal. The NAND cycle has been catastrophically wrong in both directions before, and it could turn on a supply ramp or a slowdown in AI capital expenditure.

For its part, Google has pledged up to $185 billion in AI infrastructure spending in 2026 alone. Meta directly cited rising memory pricing as the primary driver of its increased capital-expenditure guidance, while Microsoft attributed roughly $25 billion of its $190 billion 2026 capex to rising component costs, per CNBC. The hyperscalers aren’t slowing down.

Sandisk, backed by its long-running Kioxia joint venture, five multiyear customer supply agreements carrying more than $11 billion of financial guarantees, and a BiCS8 3D NAND architecture with a roadmap aimed at AI-inference memory bottlenecks, is one of the cleanest NAND/flash pure-plays on the memory side of the AI trade.

Its Q4 revenue guidance of $7.75 billion to $8.25 billion implies an annualized run rate above $30 billion—remarkable for a company that re-entered public trading a year ago at around ten bucks per share.

Disclaimer

The views and opinions expressed by the author are for informational purposes only and do not constitute financial, investment, or other advice.

Daily Debrief Newsletter

Start every day with the top news stories right now, plus original features, a podcast, videos and more.

Business#Sandisk #Mooning #Meme #Coin #Here039s1778114870

{kind=link}