Citigroup revised its near-term gold price target this week, and the smart money bought long positions before the note landed. The biggest traders were already there.

The revision was a cut from $4,300 to $4,000. Yet the perps book, the options market, and the macro backdrop had all leaned bearish for weeks. The bank confirmed the trade. It did not call it.

The Revision That Followed the Crowd

Here is the headline move. Citi lowered its near-term gold price target to $4,000 from $4,300. This could be due to expectations of higher US interest rates this year, amid the Strait of Hormuz impasse and high energy prices.

On its own, that looks like a bank turning cautious after a long rally. The mystery is the timing, because the real money had already moved the same way.

This is where positioning matters. Positioning data shows how the largest and most successful traders are placed, long or short, before the headlines catch up.

On gold, that data had been flashing Citi’s warning for weeks. The question is not why Citi cut, but how the smart money got there first.

Who Got There First, and Why It Matters

Two groups of traders moved ahead of the bank, and both warrant definitions. These are whales and smart money.

When both groups lean the same way, it is a strong signal. On the gold price, they did exactly that, well before Citi published.

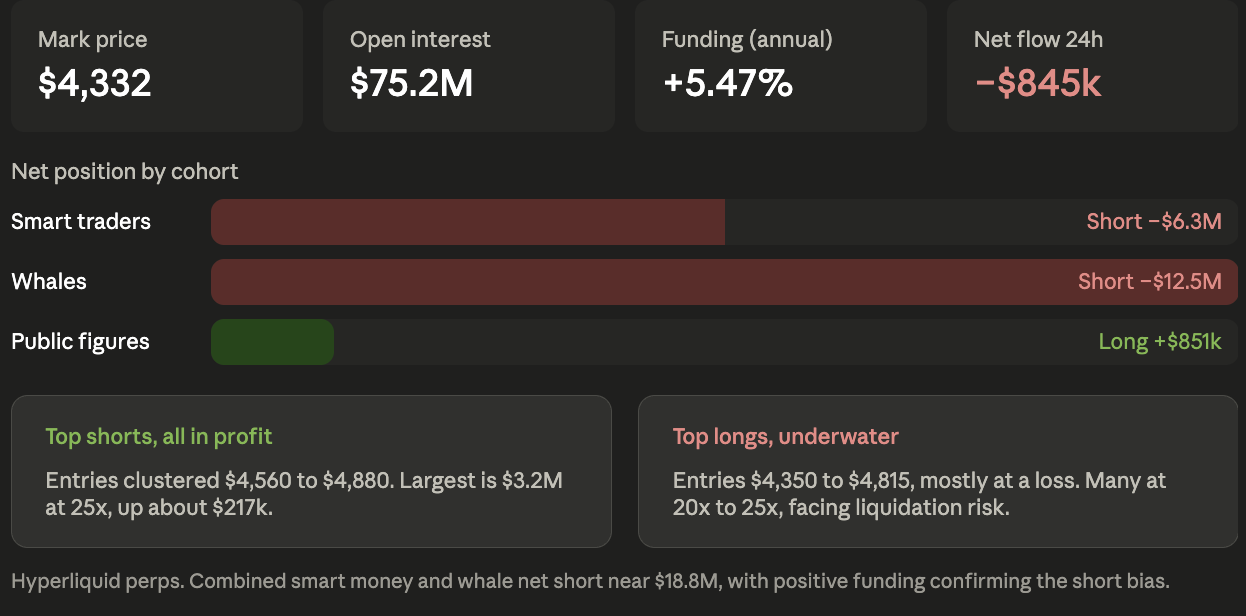

The proof sits in the perps book. On Hyperliquid, the smart money and whale cohorts are both net short gold, a combined position of nearly $18.8 million. Smart money sits short about $6.3 million. Whales lean short by $12.5 million, the heavier bet of the two.

The profit picture confirms the conviction. The top short positions entered between $4,560 and $4,880, and all sit in profit, while the largest longs entered higher up the rally and now show unrealized losses.

The funding rate seals it. At about 5.47% annualized and positive, longs are paying shorts to hold their positions, exactly what a short-dominated market looks like.

So the traders who moved first were positioned for a pullback before Citi’s note. The options market told the same story.

The Options Market Tilted Bearish Too

The signal repeats in gold’s largest ETF. The put-call ratio, which measures bearish bets against bullish ones, shifted toward puts on the SPDR Gold fund.

In early June, the volume ratio was near 0.64, and the open interest ratio was near 0.55. The open interest ratio has since risen to 0.59, while the volume ratio jumped to 1.13.

A volume ratio above 1 indicates more put contracts traded than calls. That is a clear bearish tilt, and it matches the short positioning in the perps market.

Two separate venues, the perps book and the ETF options, leaned the same way. The most regulated venue of all confirmed it next.

The COT Report Showed the Institutions Pulling Back

The heaviest signal came from the Commitments of Traders report, the weekly CFTC filing that breaks gold futures positioning down by trader type.

As of June 2, total open interest fell by 27,437 contracts to 326,052. Shrinking open interest as price weakens suggests traders are closing positions, not opening new bullish ones.

The detail matters. Large speculators trimmed their short book but added a few fresh longs, while commercial hedgers stayed heavily net short at 260,196 contracts against 53,851 long.

That mix shows conviction draining from the long side. The regulated futures market was already easing off gold before Citi published its report.

Three venues, crypto perps, ETF options, and regulated futures, all leaned bearish before Citi. The macro backdrop gave them the reason.

The Macro Backdrop Stopped Favoring Gold

Here, the pieces connect. The forces that usually lift gold had quietly turned against it.

The Treasury yield curve is firm and upward sloping, with the 30-year near 5% and the 10-year at 4.55%. Higher yields raise the opportunity cost of holding gold, which pays no income.

That ties directly to Citi’s probable reason. Rate-hike expectations are rising as Strait of Hormuz tensions and energy prices keep inflation sticky, and a firmer dollar adds more weight.

The commodity ratios agree. The gold-silver ratio near 63.6 and the gold-oil ratio near 48.4 indicate gold is not leading the complex, a risk-off surge, or strength against oil.

Every macro pointed in the same direction as the positioning did. Which is why the revision, when it came, resolved no mystery for anyone reading the flows.

Still, this is a near-term call, not a verdict on gold itself. Big banks have kept their long-term bullish view intact, and the crowded short positioning means any upside surprise could force a sharp short-covering bounce.

The mystery was never whether Citigroup turned bearish. The gold price had already told the story to anyone watching the whales.

The post Here’s How Whales Beat Citigroup to the $4,000 Gold Trade appeared first on BeInCrypto.

Commodities,Editor’s Pick,Gold (XAU) News#Heres #Whales #Beat #Citigroup #Gold #Trade1781036215

{kind=link}